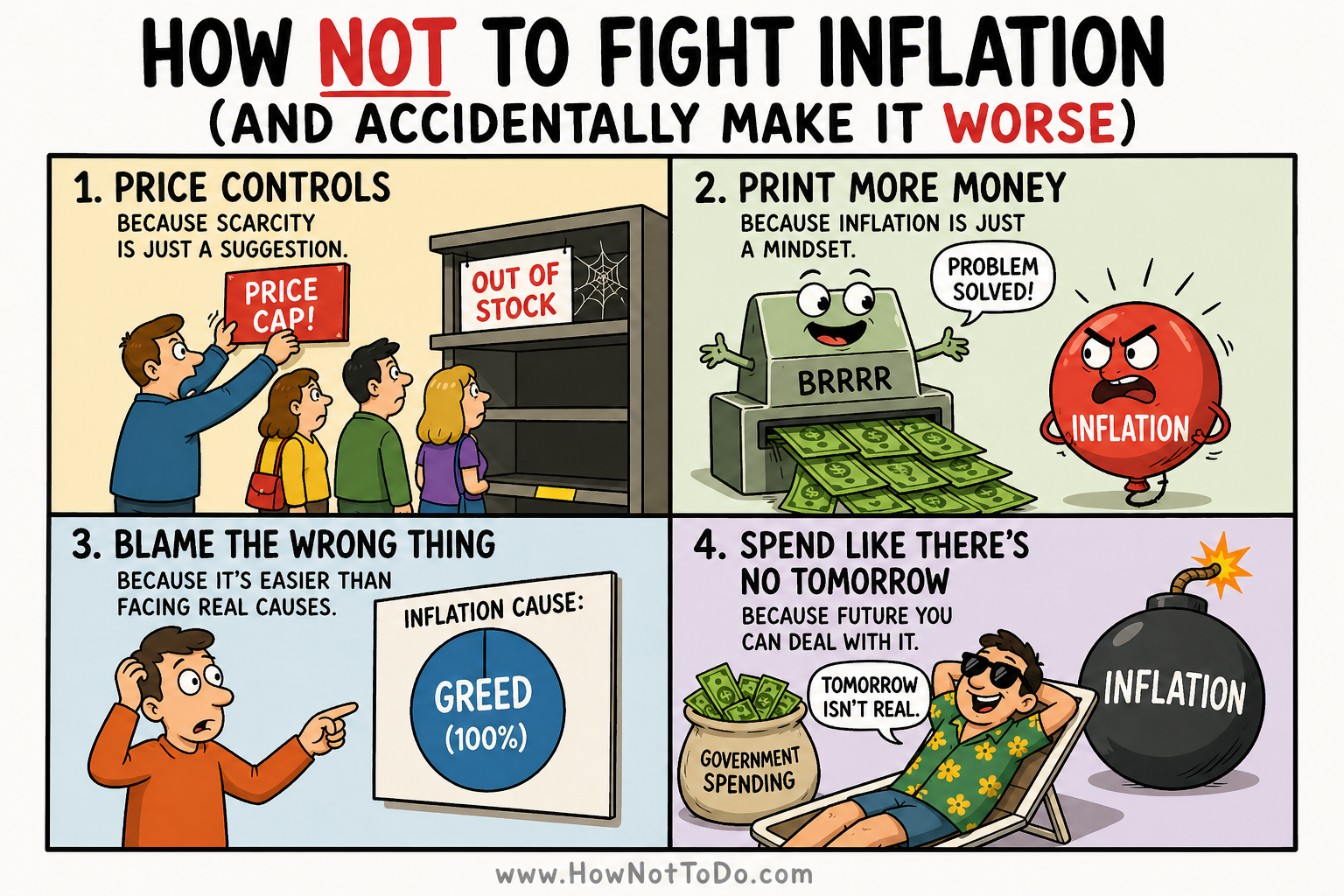

How NOT to Fight Inflation (And Accidentally Make It Worse)

Inflation is like a stealthy subscription you never signed up for. One day your groceries cost $80. The next day you’re paying $80 for the vibe of groceries.

This is not a normal “how to beat inflation” article. This is a How NOT to fight inflation guide—because the fastest way to lose money is to react emotionally, copy random TikTok strategies, and turn your entire financial life into a live experiment.

How NOT to fight inflation: the greatest hits

1) Don’t pretend it’s “temporary” for 18 straight months

The first phase is denial. You tell yourself prices will calm down next quarter. Then you keep delaying adjustments (budget, savings rate, price negotiations, subscriptions) until the “temporary” becomes your personality.

2) Don’t wage war on inflation with one heroic purchase

Buying something expensive “before it gets more expensive” feels smart. Sometimes it is. Most of the time it’s just an excuse to impulse-buy a new phone, a new car, or a 48-pack of artisanal olive oil.

3) Don’t chase returns like you’re swiping on dating apps

When inflation rises, your brain starts speed-running: “What investment beats inflation?” And then you find the guy on YouTube who says his strategy beats inflation and gravity.

4) Don’t ignore the boring tools that actually help

- High-interest debt payoff: inflation doesn’t cancel your 22% APR credit card.

- Emergency fund rules: you need liquidity so you don’t sell at the worst time.

- Automatic savings: your willpower is not an inflation hedge.

5) Don’t confuse “being busy” with “being protected”

People love busy inflation coping: tracking 17 prices across 4 stores, coupon spreadsheets, and a barter network. If it helps, great. If it consumes your life, you’ve swapped inflation for a second job you don’t get paid for.

The stealth inflation traps (that feel harmless)

Shrinkflation

The product is smaller. The price is the same. Your soul is also smaller.

Subscription creep

Inflation plus “$9.99/mo forever” is how your bank account becomes a haunted house.

Income lag

If your income doesn’t adjust, inflation is a pay cut that doesn’t ask permission.

A simple anti-inflation routine (that doesn’t require moving to a bunker)

- Once per month: review your top 10 expenses.

- Once per quarter: renegotiate 1 bill (internet, insurance, rent, phone).

- Every payday: auto-transfer a fixed amount (even small) to savings/investing.

- Weekly: one “no-spend” habit (not a punishment, just friction).

Side note: there’s a nice ebook called “The Argentine Inflation Playbook” that has real-world “inflation survival” patterns from Argentina, that can be really interesting if you are serious about fighting inflation.

FAQ (because your brain will ask anyway)

Should I keep cash during inflation?

Some cash is useful for flexibility. All cash is you volunteering as inflation’s sponsor.

What’s the one best investment to beat inflation?

If someone tells you there’s one best thing, they’re selling you the story, not the outcome.

Bottom line

Inflation punishes confusion and rewards systems. You don’t need a magical asset. You need better defaults: automation, review cadence, and fewer emotional decisions.

What NOT to do when you’re “just trying to be smart”

Most inflation mistakes don’t start with greed. They start with a reasonable thought like: “I should do something.” Then that something becomes five somethings, none of them coordinated.

- Don’t change strategy weekly: headlines are not a plan.

- Don’t buy assets you can’t explain: if you can’t describe the risk, you can’t manage it.

- Don’t ignore fees and taxes: they compound too—just against you.

- Don’t optimize tiny expenses forever: cut one big leak, then stop torturing yourself.

The “boring but effective” inflation defense stack

- Cashflow visibility: know your top 10 expenses.

- Automation: save/invest right after payday.

- Debt discipline: high APR debt is anti-wealth.

- Skill/income growth: the best hedge is getting paid more.

- Optionality: keep flexibility so you don’t sell at the worst time.

Mini scripts (because awkward money conversations are real)

- Raise: “Given costs have changed, I’d like to revisit my compensation. Here are the outcomes I delivered…”

- Bill negotiation: “I’m considering canceling. What can you do to lower the monthly price?”

- Budget boundary: “I’m not saying no forever—just not this month.”

What NOT to do when you’re “just trying to be smart”

Most inflation mistakes don’t start with greed. They start with a reasonable thought like: “I should do something.” Then that something becomes five somethings, none of them coordinated.

- Don’t change strategy weekly: headlines are not a plan.

- Don’t buy assets you can’t explain: if you can’t describe the risk, you can’t manage it.

- Don’t ignore fees and taxes: they compound too—just against you.

- Don’t optimize tiny expenses forever: cut one big leak, then stop torturing yourself.

The “boring but effective” inflation defense stack

- Cashflow visibility: know your top 10 expenses.

- Automation: save/invest right after payday.

- Debt discipline: high APR debt is anti-wealth.

- Skill/income growth: the best hedge is getting paid more.

- Optionality: keep flexibility so you don’t sell at the worst time.

Mini scripts (because awkward money conversations are real)

- Raise: “Given costs have changed, I’d like to revisit my compensation. Here are the outcomes I delivered…”

- Bill negotiation: “I’m considering canceling. What can you do to lower the monthly price?”

- Budget boundary: “I’m not saying no forever—just not this month.”

What NOT to do when you’re “just trying to be smart”

Most inflation mistakes don’t start with greed. They start with a reasonable thought like: “I should do something.” Then that something becomes five somethings, none of them coordinated.

- Don’t change strategy weekly: headlines are not a plan.

- Don’t buy assets you can’t explain: if you can’t describe the risk, you can’t manage it.

- Don’t ignore fees and taxes: they compound too—just against you.

- Don’t optimize tiny expenses forever: cut one big leak, then stop torturing yourself.

The “boring but effective” inflation defense stack

- Cashflow visibility: know your top 10 expenses.

- Automation: save/invest right after payday.

- Debt discipline: high APR debt is anti-wealth.

- Skill/income growth: the best hedge is getting paid more.

- Optionality: keep flexibility so you don’t sell at the worst time.

Mini scripts (because awkward money conversations are real)

- Raise: “Given costs have changed, I’d like to revisit my compensation. Here are the outcomes I delivered…”

- Bill negotiation: “I’m considering canceling. What can you do to lower the monthly price?”

- Budget boundary: “I’m not saying no forever—just not this month.”